The Limits of Retirement Simulators

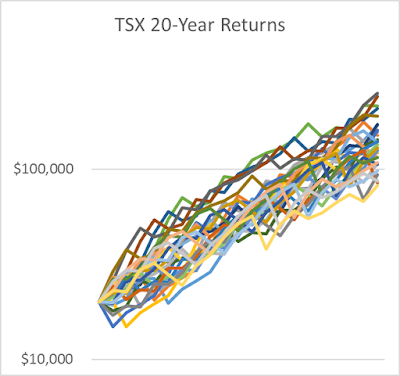

One way you can see some possible outcomes of your retirement plan is to use a retirement simulator similar to one available from Vanguard . These simulators use Monte Carlo methods to run several thousand possible patterns of investment returns to see how your portfolio holds up through retirement. Behind the impressive scientific-looking tools are some problems. Here I show the problems in pictures. To understand these problems, we need to look at the fairly simple way these simulators work. To generate a possible outcome for your portfolio, many of these simulators begin with some actual historical investment returns from a range of years. They build your simulated results one year at a time by choosing one of the historical years randomly and applying that year’s returns to your portfolio. Before getting into why this method has some issues, let’s go to a couple of charts. I grabbed some annual TSX investment returns for the past 47 years. Then I made a chart of portfoli...