Short Takes: Bond Surprise and Sticking to a Plan

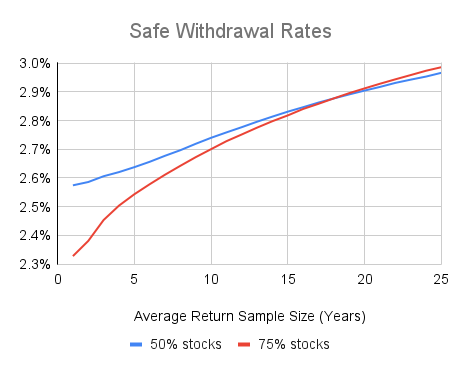

When people suggest topics for me to write about, more often than not I can point to an article I’ve already written, which is handy for me. I doubt I’ll ever run out of thoughts on new topics, but it’s good to have a body of work to refer to. Here are my posts for the past two weeks: Car Companies Complaining about Interest Rates RRSP Confusion Searching for a Safe Withdrawal Rate: the Effect of Sampling Block Size Here are some short takes and some weekend reading: Ben Carlson lists some things in the markets that surprised him this year. The first thing is that stocks and bonds both went down double-digits. Apparently, that’s never happened before. I guess if you just look at the history of stock and bond returns, this outcome looks surprising. However, when you look at the conditions we’ve come through, this was one among a handful of likely outcomes. Bond markets were being artificially propped up, and the dam had to burst sometime. As for...