Short Takes: Empty Return Promises, Asset Allocation ETFs, and more

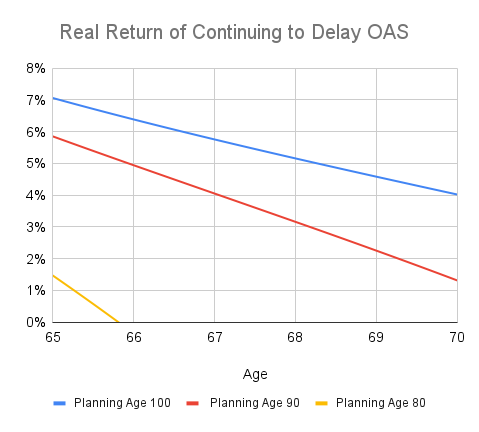

I came across yet another case of a furious investor whose advisor had promised a minimum return, but the portfolio lost money. There is a lot wrong with this picture. On the client side, they often believe that advisors have some meaningful level of control over returns and that advisors can somehow steer around bear markets, which is nonsense. Advisors can choose a risk level. The only way to guarantee a (low) return is to take little or no risk. On the advisor side, I can only assume that many advisors are under so much pressure to land clients that they make promises they know they can’t keep unless they get lucky. All the while, the management above these advisors know full well what is going on. Here are my posts for the past four weeks: Giving With a Warm Hand The Case for Delaying OAS has Improved Here are some short takes and some weekend reading: Robb Engen at Boomer and Echo sings the praises of Vanguard Canada’s Asset Allocation ETFs....